Nepal’s energy sector stands at a pivotal moment in its history, carrying both the legacy and momentum of an industry that has reshaped the nation’s economy. In just one generation, the country has moved from enduring eighteen-hour power outages to achieving a wet-season energy surplus. It has also begun taking its first steps toward cross-border electricity trade.

That progress came through steady resolve amid difficult terrain and shifting politics. Uneven regulation also played a part. The journey ahead is uncertain. Reaching the national goal of 28,500 MW by 2035 will not be straightforward. It demands careful judgment in the face of a widening crisis. Unclear domestic policies and climate-driven changes in river flows intersect with delicate regional power politics. Nepal holds a unique opportunity to move beyond exporting electricity as a raw commodity. The country can position itself as a Green Digital Bridge for South Asia, linking its surplus hydropower with the growing energy demands of global artificial intelligence infrastructure and opening a new chapter of economic growth. Yet, these potential faces significant hurdles. Domestic constraints continue to slow progress, including regressive provisions in power purchase agreements and unresolved disputes over industrial tariffs between the Nepal Electricity Authority and private producers. The prolonged legislative deadlock over the Electricity Bill 2080 further complicates the path forward. Until these challenges are addressed, Nepal’s broader energy vision will remain difficult to realize.

The Genesis and Evolution of IPPAN (2001–2026)

The Independent Power Producers’ Association, Nepal (IPPAN), was founded on Magh 4, 2057 BS by eight pioneers at a time when private participation in hydropower was widely questioned. Energy development was then considered a state monopoly, with the Nepal Electricity Authority controlling generation, transmission, and distribution. Early private developers faced significant hurdles in obtaining licenses and grid access. The association grew over the twenty-five years and now represents more than 506 corporate members. This expansion reflects a fundamental transformation in the power sector.

Independent producers now generate the bulk of Nepal’s electricity, contributing over 3,203 MWh to the grid compared to 582 MWh from the state. Control of key national infrastructure has largely shifted from public oversight to private hands—a transition formally commemorated by the association during its Silver Jubilee in January 2025.

Domestic constraints continue to slow progress, including regressive provisions in power purchase agreements and unresolved disputes over industrial tariffs between the Nepal Electricity Authority and private producers. The prolonged legislative deadlock over the Electricity Bill 2080 further complicates the path forward. Until these challenges are addressed, Nepal’s broader energy vision will remain difficult to realize.

The mobilization of domestic capital stands as a primary outcome of this era. Hydropower attracted billions in local equity and debt while other sectors remained dependent on foreign aid. Public share offerings enabled ordinary citizens to participate as direct investors. This structure created a rare economic model where the public serves as both consumer and financier. Success has fostered comfort with current market assumptions. The sector faces a test of these premises by 2026 as it confronts the limitations of the river-based generation model.

The Urja Samriddhi Vision and the 2035 Roadmap

The concept of Urja Samriddhi is the primary directive for the coming decade. The government formalized this ambition in the Energy Development Roadmap and Action Plan 2081 as the most significant objectives the nation has ever recorded. The plan centers on increasing installed power capacity to 28,500 MW by the year 2035.

The success of this ambition will alter the fundamental structure of the national economy. The targets indicate that the administration seeks two simultaneous outcomes. One objective is the construction of a domestic industrial base. The second is the establishment of Nepal as a significant exporter of electricity. Authorities have estimated 13,500 MW of the total capacity for internal consumption. They have allocated the remaining 15,000 MW for sale to foreign markets.

The magnitude of this requirement has no precedent. Attaining these objectives necessitates rates of expansion that exceed all prior achievements in the sector. The effort also demands an estimated USD 46.5 billion in capital investment over the next decade. This sum surpasses the current annual Gross Domestic Product of Nepal. Energy must therefore become the principal attraction for foreign investment and a primary recipient of global climate finance. The strategic plan acknowledges this necessity. It includes provisions to secure USD 2 billion from climate funds. It further aims to obtain USD 8.5 billion through foreign loans.

The vision of Urja Samriddhi is approaching a critical juncture as 2026 nears. While the government has articulated its objectives clearly, regulatory hurdles and legislative delays continue to hamper the administrative machinery needed to advance the sector. The widening gap between political intent and administrative execution remains the principal challenge to Nepal’s energy transition.

The sector’s heavy reliance on run-of-river projects creates an uneven generation profile—power surges during the monsoon from June to September but drops sharply in winter, producing a recurring firm power gap. Nepal imports electricity from India during dry months even as it breaks export records in summer.

The Hydrological Foundation and Climate Vulnerability

Nepal’s energy future hinges on the river systems of the Koshi, Gandaki, and Karnali basins. With over 6,000 rivers and an estimated potential of 83,000 MW, the country’s hydropower capacity is immense. Yet, planners can no longer rely on historical river patterns: climate change has introduced unprecedented uncertainty. Floods in late 2025 damaged several operating and under-construction plants, exposing the sector’s vulnerability and prompting IPPAN to seek immediate reconstruction relief. Climate resilience is now a direct financial concern, influencing both balance sheets and investor confidence.

The sector’s heavy reliance on run-of-river projects creates an uneven generation profile—power surges during the monsoon from June to September but drops sharply in winter, producing a recurring firm power gap. Nepal imports electricity from India during dry months even as it breaks export records in summer. Achieving the 2035 targets will require a deliberate shift toward storage-based generation, a transition demanding advanced technical capacity and significant capital investment.

Sharp policy uncertainty defined the period from late 2025 into early 2026. The energy sector became a focal point of regulatory strain. This occurred even with the political continuity provided by the interim government of Prime Minister Sushila Karki. The 2025/26 fiscal policy presented the primary threat to the 28,500 MW roadmap. The government reintroduced a Take and Pay clause in Power Purchase Agreements. This decision weakened the investment climate for hydropower.

The traditional Take or Pay model has been the foundation of project financing for decades. The Nepal Electricity Authority guarantees payment for all electricity generated under this framework. It provides this guarantee whether or not it can transmit or consume the power. This assurance allows banks to fund capital-intensive projects. The shift to Take and Pay means the utility pays only for the electricity it receives. This arrangement transfers market and transmission risks to the private developer. The consequences are grave. Lenders argue that projects under Take-and-Pay terms are unfinanceable, as revenue streams are not guaranteed. IPPAN warns that around 17,000 MW of projects could face indefinite suspension. While the Ministry of Energy depends on private investment to achieve its roadmap, the Ministry of Finance has removed the financial security needed to attract it. IPPAN President Ganesh Karki called this approach unrealistic, warning it threatens long-term energy security. The policy safeguards the utility’s balance sheet at the expense of national growth, exposing a broader lack of government confidence in infrastructure delivery. By effectively acknowledging potential failures in completing transmission lines or securing export markets, the state signals its unwillingness to bear the cost of those failures.

The Industrial Dispute

The Dedicated Feeder and Trunk Line dispute has significantly strained relations between the Nepal Electricity Authority and major industrial power consumers, threatening the stability of Nepal’s energy sector. Originating during the load-shedding era and intensifying in late 2025, the conflict escalated after the NEA cut power to large factories over disputed unpaid bills. Although a payment plan was negotiated, tensions remain, underscoring how industrial slowdowns reduce electricity demand and create surplus power—highlighting the need for a strong industrial base to ensure a sustainable energy system.

Legislative Stagnation

Nepal’s energy sector reform is stalled due to delays in passing the Electricity Bill 2080, which would introduce competition by breaking the state utility’s monopoly and separating generation, transmission, and trading. Political resistance and union opposition have halted progress, leaving national power expansion targets unrealistic since the utility alone lacks the financial capacity to achieve them.

The Digital Opportunity

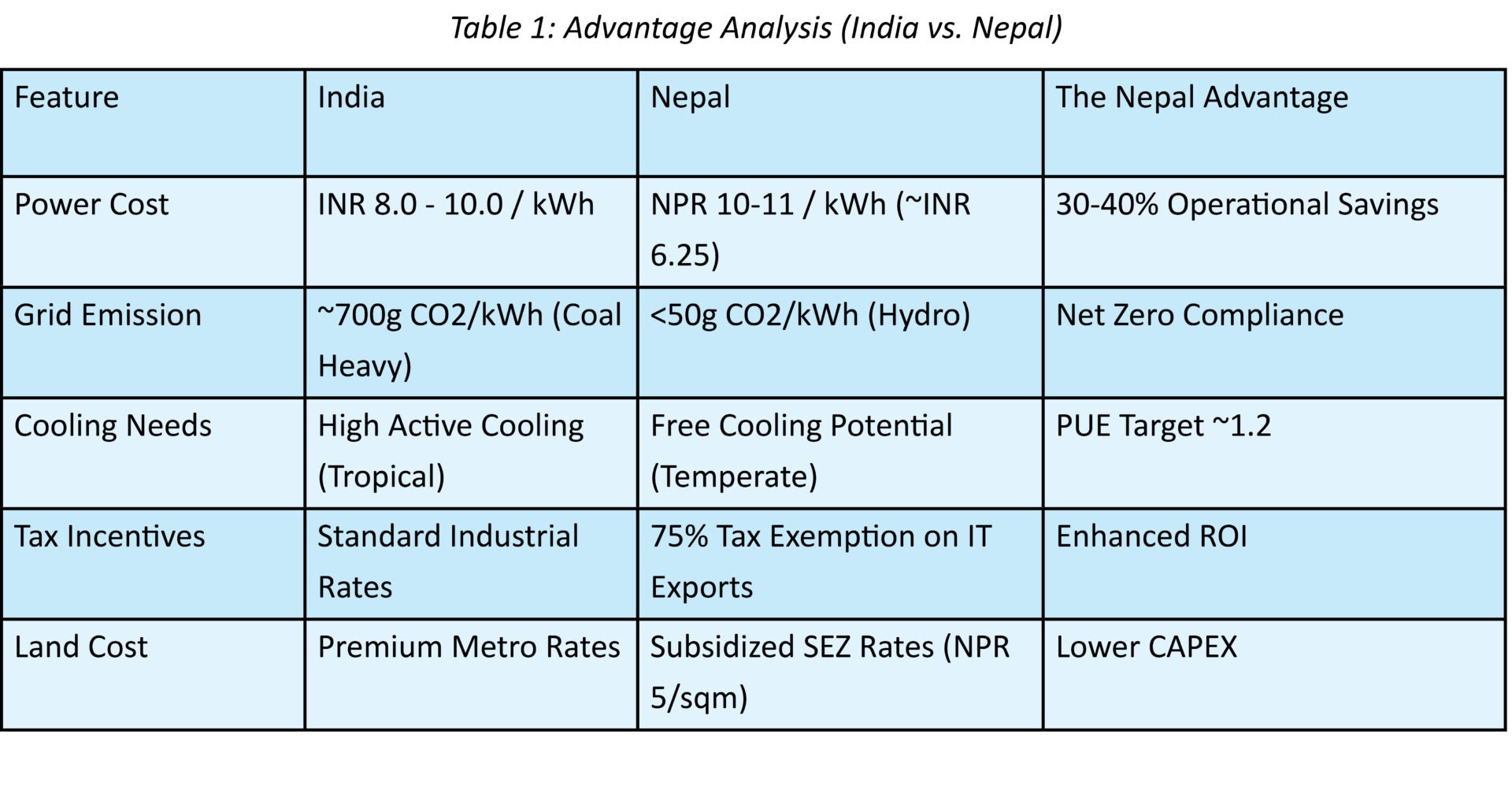

Nepal has a unique chance to leverage its renewable energy surplus amid domestic policy gridlock. The rise of Artificial Intelligence is driving soaring demand for electricity, particularly for data centers that power and cool large AI models. The International Energy Agency projects electricity demand from such facilities will double by 2026. India, with its rapidly growing digital economy—potentially reaching USD 1 trillion by 2035—faces an energy challenge, as nearly 70% of its grid is coal-powered. Global tech companies, committed to Net Zero emissions, must either purchase costly credits or build their own clean energy sources. High electricity costs and inefficiencies in Indian cities like Mumbai and Chennai create a compelling opportunity for Nepal. By exporting green energy, the country could support the region’s next wave of digital infrastructure while capitalizing on its renewable advantage.

The success of the past twenty-five years is clear. But the methods that built 3,000 megawatts will not suffice to build 28,000. The sector must change in three specific ways. It must move from quantity to quality. Adding capacity is not enough. The system requires storage and firm power. The focus must shift from construction to the market.

The Digital Bridge Strategy

Nepal offers a strategic answer to the capacity challenges facing Indian data centers. The nation holds the potential to serve as a green digital conduit for the region. The economic justification is clear. Industrial electricity in Nepal costs approximately ten Nepali rupees per unit. This price is thirty to forty percent lower than rates in Mumbai or Noida. The advantage extends beyond simple cost. The Nepali grid relies almost entirely on renewable hydroelectric power. This offers a direct method for corporations to lower their carbon emissions. The combination of affordability and sustainability makes Nepal a logical alternative for digital infrastructure.

The nation does not compete with Mumbai for high-speed financial trading. It is positioned to serve the artificial intelligence sector of northern India. Major cities such as Lucknow and Patna are geographically closer to the Nepali border than to the coastal hubs of India. This proximity creates a measurable advantage in data transmission speed. Nepal can provide faster service to the populous Gangetic plain than traditional Indian centers. The government has begun to lay the groundwork for this transformation. The Data Center and Cloud Service Directives of 2025 established a clear regulatory framework. They set Tier 3 standards and safeguarded data sovereignty. The Budget for 2081/82 introduced a fiscal incentive of a seventy-five percent income tax exemption on revenues from IT service exports. These policies open a new business model for independent power producers. They can supply power locally to data centers rather than exporting raw electricity to India where transmission losses and low tariffs reduce returns.

Connectivity has also improved. Nepal now possesses redundant optical fiber links to India through Tata and Airtel and to China via China Telecom. This redundancy removes the historical risk of single-point failure. It meets a critical requirement for hyperscalers that demand near-perfect uptime.

Storage and Hydrogen

The first twenty-five years of private power development focused on run-of-river projects. The next decade must focus on water storage. The limitations of river-based plants pushed energy storage to the forefront of the 2026 agenda. Nepal generates surplus power in the summer but faces deficits in the winter. Storage provides the only practical way to balance this seasonal swing.

Pumped Storage Hydropower emerges as the most viable large-scale solution. It uses surplus energy during off-peak hours to pump water to an upper reservoir. The water is released during peak demand. These systems function as massive water batteries. IPPAN advocates for viability gap funding to make these projects feasible. Battery Energy Storage Systems also play a role. They address short-term grid stability and frequency regulation. The decline in battery costs in 2026 makes this technology essential for integrating solar power into the national grid.

Green hydrogen offers another solution for wasted energy. Hundreds of megawatts go unused at night during the monsoon because demand is low. Nepal has the potential to produce some of the cheapest hydrogen in the world due to the low marginal cost of this spill energy. Producers can generate hydrogen or green ammonia for export or fertilizer production. This infrastructure acts as insurance. If the utility refuses to purchase electricity, electrolyzers can absorb the surplus.

Regional Integration

Meeting the export target of 15,000 MW depends on close integration with the Indian power grid. The experience of 2025 and 2026 shows that this relationship is uneven. Nepal continues to export electricity during the summer. The winter months reveal a reliance on Indian imports. The authority purchased power at high rates in early 2026. This reflects the tight conditions of the Indian market. Producers face seasonal pricing volatility. They export at competitive rates in the wet season and import at a premium in the dry season.

The process for Indian approval of hydropower imports remains strict. It often requires assurances that no Chinese investment is involved. This geopolitical due diligence adds a layer of compliance complexity. There are signs of stabilization. Export approvals were renewed for 283 MW. New projects were added to the Indian day-ahead market.

A major development is the start of power exports to Bangladesh. Nepal began supplying 40 MW using Indian transmission infrastructure. The volume is modest compared to exports to India. The strategic significance is considerable. It offers a chance to diversify markets. Reducing reliance on a single buyer is critical for establishing fairer pricing. The tripartite agreement provides a model for future sub-regional grid integration.

Domestic Demand and Capital

The roadmap goal of 13,500 MW for domestic consumption by 2035 requires a transformation of demand. Electric vehicles offer the fastest path to absorb surplus power. Infrastructure development has lagged. Europe and China deploy ultra-fast charging networks at scale. Facilities in Nepal remain patchy. Expanding public charging networks must be a priority for 2026. Charging stations should be treated as national priority projects with subsidized land and electricity tariffs. Most charging occurs at night. This provides steady demand for run-of-river projects.

The industrial sector is also ready to switch from coal and diesel to electricity. This can happen only if the supply is reliable. The dispute over dedicated feeders highlights the problem of power quality. Frequent tripping forces factories to rely on costly diesel backups. The utility must invest in grid modernization to deliver industrial-grade power. Factories can replace thermal boilers with electric ones only with consistent electricity.

Meeting the 2035 vision requires an investment of nearly forty-six billion dollars. Domestic capital is insufficient. Foreign direct investment is essential. Currency risk remains a major deterrent. The fluctuation between the rupee and the dollar causes investors to demand high risk premiums. The sector needs a government-backed hedging fund to subsidize the cost of this risk. Nepal also has a marketing asset in its low-carbon grid. Renewable Energy Certificates provide a way to monetize this green status. A data center in Mumbai or a factory in Europe could purchase these certificates to offset their carbon footprint. This generates hard currency revenue without relying on cross-border transmission lines.

The Road Ahead

The next decade of energy development demands a practical approach. IPPAN Day 2026 signals a time for careful ambition. The success of the past twenty-five years is clear. But the methods that built 3,000 megawatts will not suffice to build 28,000. The sector must change in three specific ways. It must move from quantity to quality. Adding capacity is not enough. The system requires storage and firm power. The focus must shift from construction to the market. Building dams is less critical than trading power and creating demand. The reliance on river flow must end. A balanced mix of solar and storage is necessary. The government has a duty to fix the policy errors of 2025. The Take and Pay rule must be repealed. The Electricity Bill needs to pass to free the private sector. Nepal holds a resource that the world requires. Clean energy is in short supply. Linking this power to the digital economy offers a chance for real wealth. This prosperity can flow as surely as the rivers.

(Chaudhary is the Vice President of the Independent Power Producers’ Association of Nepal (IPPAN), and Bhattarai is the Associate Director at the Asian Institute of Artificial Intelligence and Co-Convenor, Startup & Private Equity Committee, Nepal-India Chamber of Commerce and Industry)

References

Independent Power Producers’ Association, Nepal, accessed on January 4, 2026, https://storageasia.solarenergyevents.com/sponsor/independent-power-producers-association-nepal/

Independent Power Producers’ Association, Nepal – Official Website …, accessed on January 4, 2026, https://www.ippan.org.np/

Report – Independent Power Producers’ Association, Nepal, accessed on January 4, 2026, https://www.ippan.org.np/wp-content/uploads/2025/04/Ippan-Day-Pratibedan-2081_English.pdf

Nepal’s energy plan: A pathway to sustainable development, accessed on January 4, 2026, https://www.ippan.org.np/6248

Nepal’s Energy Sector Development: A Vision for Prosperity and …, accessed on January 4, 2026, https://nepsetrading.com/blog/nepals-energy-sector-development-a-vision-for-prosperity-and-regional-cooperation

IPPAN welcomes energy roadmap, demands policy reforms, accessed on January 4, 2026, https://risingnepaldaily.com/news/55238

It is feasible to generate 28,500 MW electricity by 2035, accessed on January 4, 2026, https://risingnepaldaily.com/news/55181

IPPAN demands relief for flood-hit hydro projects – The Rising Nepal, accessed on January 4, 2026, https://risingnepaldaily.com/news/69432

IPPAN commits to collaborate with new government in energy sector, accessed on January 4, 2026, https://risingnepaldaily.com/news/68261

Nepal’s energy sector rocked by ‘take-and-pay’ budget policy, accessed on January 4, 2026, https://kathmandupost.com/national/2025/06/05/nepal-s-energy-sector-rocked-by-take-and-pay-budget-policy

IPPAN Protests Retention of ‘Take and Pay’ Provision in Budget, accessed on January 4, 2026, http://www.nepalenergyforum.com/ippan-protests-retention-of-take-and-pay-provision-in-budget/

IPPAN President warns govt policy could force hydropower shutdowns, accessed on January 4, 2026, https://english.khabarhub.com/2025/04/473840/

Private sector body announces compromise on power bill dispute, accessed on January 4, 2026, https://kathmandupost.com/national/2025/11/04/fncci-announces-compromise-on-power-bill-dispute

Industrialists on warpath again as Ghising continues to cut power …, accessed on January 4, 2026, https://kathmandupost.com/national/2025/10/26/industrialists-on-warpath-again-as-ghising-continues-to-cut-power-supply

Electricity Bill Stalled in Parliamentary Committee for 18 Months, accessed on January 4, 2026, http://www.nepalenergyforum.com/electricity-bill-stalled-in-parliamentary-committee-for-18-months/

CORPORATE DEVELOPMENT PLAN – energypedia, accessed on January 4, 2026, https://energypedia.info/images/c/c7/NEA_Corporate_Development_Plan.pdf

A Research Report in AI Data Centre Investment.pdf

IPPAN at Energy Storage Summit 2026!, accessed on January 4, 2026, https://www.ippan.org.np/6846

IPPAN at 3rd Edition Energy Storage Australia 2026, accessed on January 4, 2026, https://www.ippan.org.np/6853

NEA Board Decided to Open PPA for 1015 MW Solar and up to 10 …, accessed on January 4, 2026, https://www.urjakhabar.com/news/1202780688

INTERNATIONAL CONFERENCE ON GREEN HYDROGEN 2025, accessed on January 4, 2026, https://icgh.in/

Case for a Global Green Hydrogen Alliance, accessed on January 4, 2026, https://globalgovernanceforum.org/wp-content/uploads/2023/07/Case-for-a-Global-Green-Hydrogen-Alliance.pdf

Nepal Electricity Authority (NEA) and PTC India sign agreement to …, accessed on January 4, 2026, https://laganinews.com/en/2025/11/25/nepal-electricity-authority-nea-and-ptc-india-sign-agreement-to-export-electricity-what-happened-on-what-date-2/

Nepal Must Ramp Up Electricity Production Amid Rising Indian …, accessed on January 4, 2026, http://www.nepalenergyforum.com/nepal-must-ramp-up-electricity-production-amid-rising-indian-demand/

Electric vehicle charging – Global EV Outlook 2025 – Analysis – IEA, accessed on January 4, 2026, https://www.iea.org/reports/global-ev-outlook-2025/electric-vehicle-charging

IPPAN President Ganesh Karki urges Indian investors to invest in …, accessed on January 4, 2026, https://en.nepalkhabar.com/news/detail/13214/